Chicago’s Suburban Office Market:

More Competitive Than You Think

Headlines have declared the death of the suburban office market.

Even our data may appear to support this claim, with the overall market posting a 27.6% vacancy rate as of September 2021—a 26% increase from the end of Q4/19, a timeframe that correlates directly with the global pandemic. Clearly, the pandemic decimated the suburban office market… or did it? Our on-the-ground reconnaissance reveals the market is tighter than the aggregate rates and the headlines suggest. In fact, we find average vacancy rates are skewed higher, due to large, functionally obsolete buildings, many empty for more than five years.

What the pandemic has done–across many sectors of the economy, not just commercial real estate–is exacerbate economic trends already in place. And there may not be a more secular trend than high-quality properties attracting tenants and low-quality properties losing them.

To test our hypothesis, we divided the suburban office market inventory into the most-occupied (top quartile) and least-occupied (bottom quartile) buildings. We’re calling the most-occupied buildings (> 90% occupancy) the Market Leaders and the least-occupied buildings (< 37% occupancy) the Market Laggards. As Exhibit 1 illustrates, the occupancy trends were in place as far back as 2011, well before the pandemic.

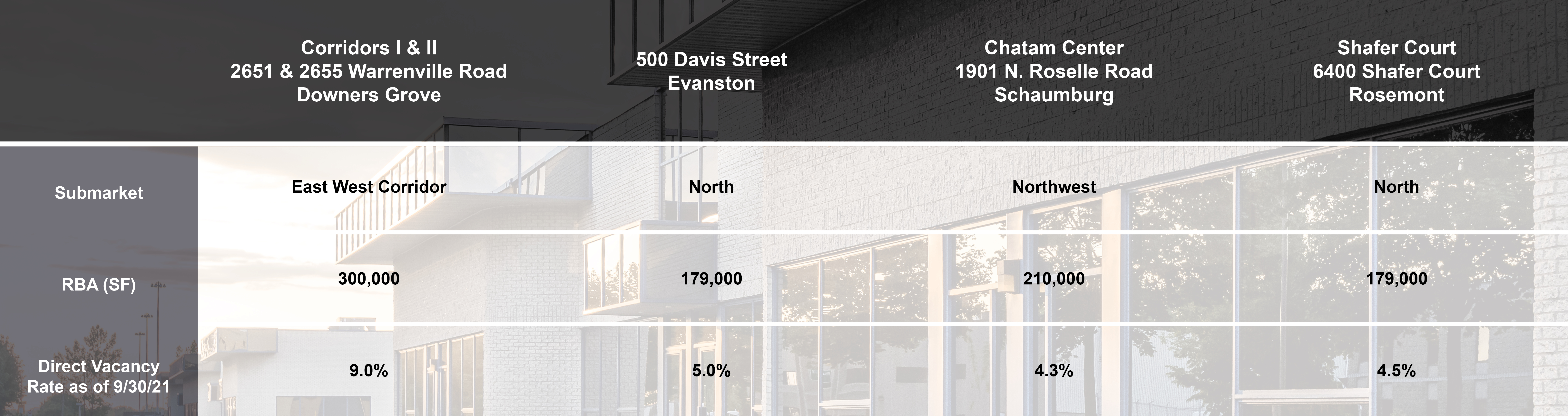

For the Leaders, vacancy rates have been on steady decline for a decade, and three-fourths of the way through 2021 the vacancy rate for these properties fell to 4.3%—the lowest in more than 10 years (see Exhibit 2 for representative examples).

Exhibit 2: Representative Market Leaders

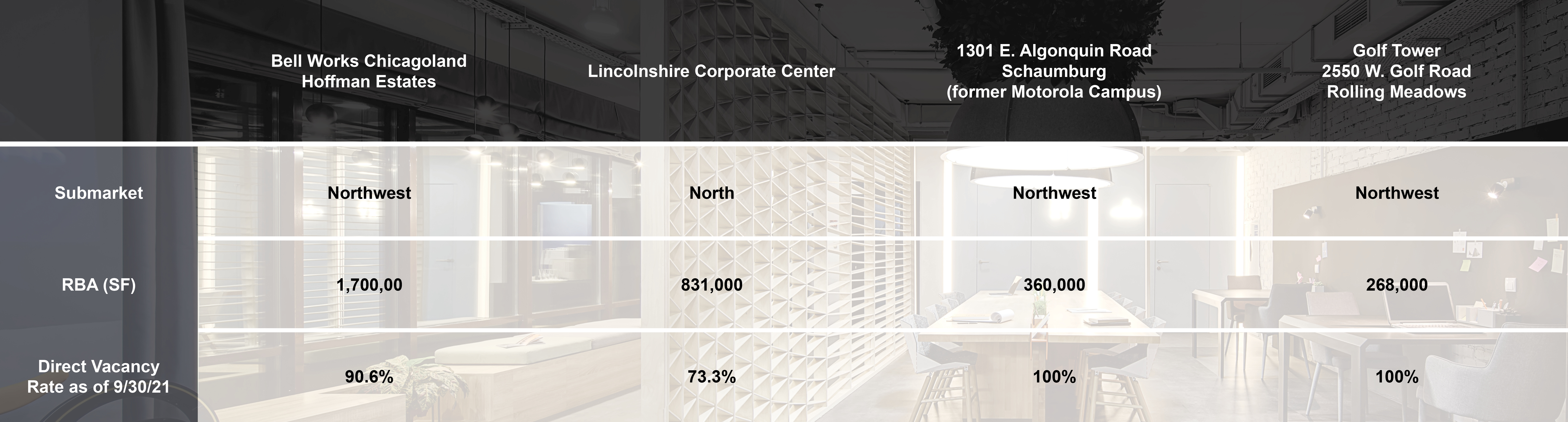

Vacancy rates for the Laggards, on the other hand, have been increasing for the past decade, especially over the past five years. Clearly, this group was struggling long before the Covid-19 economic standstill. Thirty-one “zombie” office buildings—with 100,000+ s.f. of vacant space—continued to drag the overall outlook of the region’s office supply (see Exhibit 3 for representative examples).

Exhibit 3: Representative Market Laggards

Exhibit 4: Suburban Chicago Office Market Less the Laggards

To be sure, the pandemic extracted enormous costs from a variety of industries. Businesses in the retail and the arts and entertainment spheres needed to pivot to get through this health crisis and thrive in the new world. Many made it to 2021; many did not. The same is true in commercial real estate. The trophy office of today may be the eyesore of tomorrow. From our vantage point, the buildings that struggled through the pandemic were already struggling before the pandemic. Landlords, like other business owners, need to take a hard look at their assets’ life cycles. Is it cost prohibitive to demise the property to meet the needs of the modern tenant? Is the location desirable and near transportation arteries? The decision to defer sizable capital improvements may lead to a languishing future for an asset. With good bones and a great location, however, landlords can also pivot and rewrite a new future for their assets, as many did during the past year. For example, through renovations over the past five years, AT&T’s former campus at Bell Works Chicagoland and Motorola’s former campus at Schaumburg Towers (formerly on the Laggards list) were able to secure new tenants across multiple deals for a total 89,000 s.f., all in just the past four months (see Exhibit 5 below).